Most people who are eligible for coverage offered on the Affordable Care Act (ACA) marketplace do not know when they can sign up for insurance. Open enrollment, the time period during which people can enroll in private plans offered on the marketplace, begins on November 1.

The Kaiser Family Foundation (KFF), a leading health policy analysis center, reported its new findings on Wednesday. A majority of uninsured people did not know either when open enrollment begins (85 percent) or ends (95 percent). A significant majority of those currently enrolled in the marketplace also do not know when it begins (59 percent) or ends (75 percent).

The newly released polling data comes as health policy in Washington, D.C. fluctuates minute-by-minute. Within a 24-hour time period last week, President Donald Trump issued an executive order aimed at hobbling the ACA and cut key subsidy payments to insurance companies, further solidifying his intention to undermine current health law. The news prompted legislative action by Congress, but has also confused consumers in the process.

The report also confirms what Rhonda Henry, founder of the ACA Signup Project, has been witnessing firsthand. Many people have been confused about the current health law since the last G.O.P. health bill failed in the Senate mid-September.

“There’s a lot of things to be confused about especially if you haven’t been following this as a geek, wonk person,” Henry told ThinkProgress.

It doesn’t help that the federal marketplace’s greatest and much-needed advertiser has been purporting misleading facts about where the current health law stands.

Last Thursday, Trump said he would stop making cost-sharing reduction (CSR) payments necessary for the ACA. On Monday, Trump said “there’s no such thing as Obamacare anymore.” (There is. Again, open enrollment begins on November 1.) On Tuesday, Trump said he was in support of a bipartisan deal in Congress that would reinstall the cost-sharing reduction payments that he himself decided not to make a few days earlier. But by Tuesday night, he disavowed the payments again, claiming during a speech at the Heritage Foundation that “Congress must find a solution to the Obamacare mess instead of providing bailouts to insurance companies.” (Republicans who voted against the Obamacare repeal bill in September, known as the Graham-Cassidy bill, are mostly happy with the bipartisan Senate bill and have said it’s not an insurer bailout.)

Health care is complicated. Thankfully, for people who are looking to sign up for coverage on healthcare.gov or on their own state’s ACA exchange (California’s exchange, for example is Covered California), it doesn’t need to be. There have been some changes that people who enroll for coverage in two weeks need to take note of.

The first, is premiums are increasing, but the majority of ACA enrollees will not notice.

“We know premiums are increasing in large part because of the Trump administration actions like cutting cost sharing reduction payments,” Kaiser Family Foundation’s Senior Vice President of Special Initiatives Larry Levitt told ThinkProgress and other reporters during a press call on Wednesday.

According to the KFF poll, about half of the marketplace enrollees expect premiums increases in 2018 will be a financial burden. And it could be, but only for people who receive care without federal assistance. Of the 12.2 million people who buy insurance on the ACA marketplace, 83 percent (or 10.1 million) qualify for federal premium subsidies.

In California, insurance companies anticipated that the federal government would not pay them for providing cost sharing reduction subsidies (CSR), or money that helps low-income people pay for out-of-pocket health expenses. To offset financial losses, insurers increased premiums for silver-tier plans, a standard ACA health plan that offers CSRs.

For a 30-year old in Sacramento, California who makes $24,120 in 2018, they will likely see a $130 premium for a benchmark silver plan, a three dollar increase from last year. Although the premium increased from $378 in 2017 to $425 dollars in 2018, the premium subsidy increased as well, safeguarding the consumer and increasing the federal government’s tab.

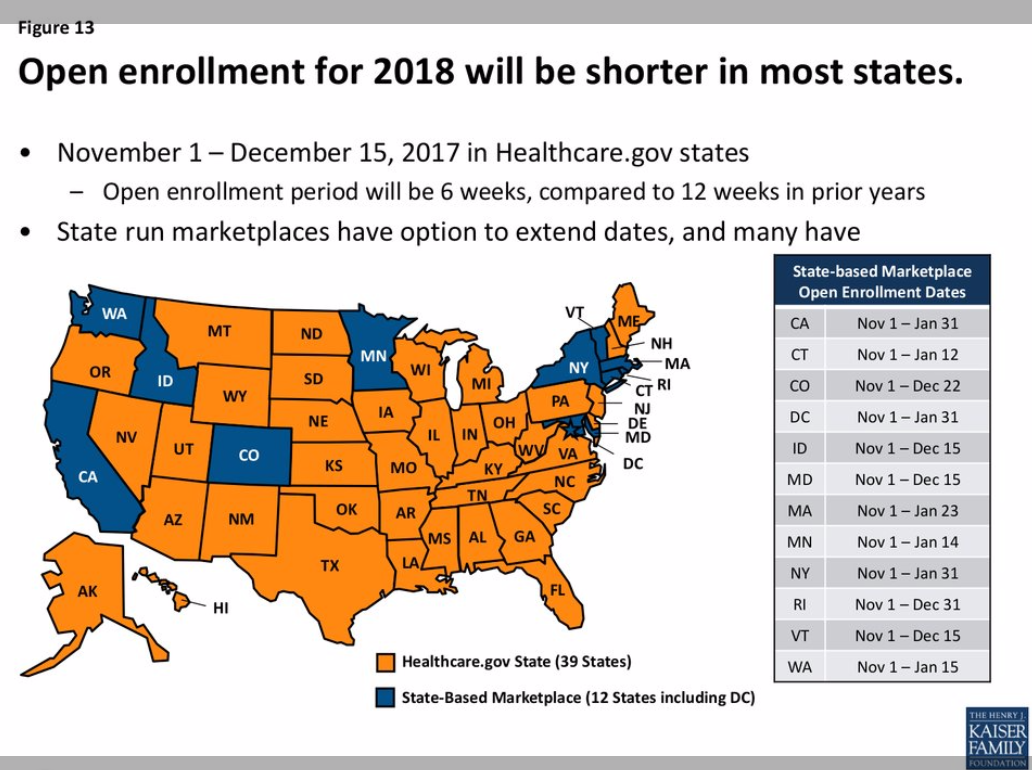

Another change of note for consumers who buy ACA plans is that open enrollment will be shorter than last year if the state operates on healthcare.gov. Every state’s open enrollment period begins on November 1, but 42 states will see it end 6 weeks earlier than last year.

Additionally, there will be planned maintenance on healthcare.gov during open enrollment. If heathcare.gov isn’t working Sundays from midnight to noon, that’s why.

This will be a more challenging enrollment year, Covered California Spokeswoman Lizelda Lopez told ThinkProgress.

“The news is changing every five minutes about what federal government might do, and we are trying to explain to our consumers to stay calm,” said Lopez. Covered California has been sending clarifying emails to consumers every time news breaks.

According to KFF polling, a key reason people do not know about open enrollment is because many have seen few advertisements. The Trump administration cut funding for ACA advertisement by 90 percent.

“It’s certainly not helping,” the director of state health reform for the Kaiser Family Foundation Jennifer Tolbert said on the press call Wednesday. “What we know is consumers need to hear this information over and over again.”