The anti-climate policies embraced by President-elect Donald Trump— coupled with the ever-more stunning news and analyses that keep coming about the polar regions — means trillion-dollar economic impacts from climate change are closer at hand than people realize. Here’s why.

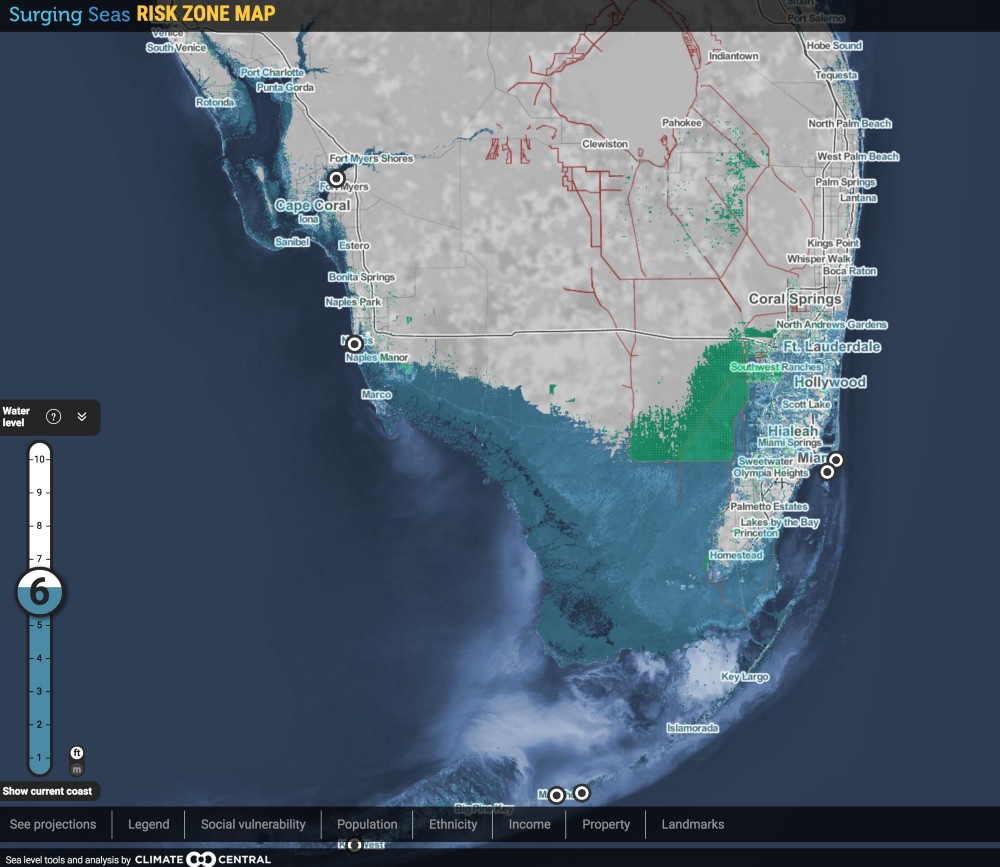

First, a new Nature study finds the Greenland ice sheet is as unstable as the Antarctic ice sheet and prone to rapid melt. It adds to the fast-growing body of evidence we are headed toward the high-end of sea level projections, up to 6 feet or more by century’s end (and you can throw in another 2 feet for the highest tides if you live in South Florida).

Second, we already knew that meant devastating Sandy-level storm surges will become more and more common on the East Coast, where sea level rise is the fastest.

Third, unusually warm weather has been driving record ice melt this year (which in turn causes more warming and more melting in an amplifying feedback called “Arctic Amplification”). Last month, Arctic sea ice extent and volume hit record lows for November. As Rutgers climatologist Jennifer Francis told the AP, “There’s crazy stuff going on up there. It’s bad.”

Therefore, only very aggressive cuts in carbon pollution could plausibly save our major coastal cities and avoid a trillion-dollar housing bubble crash

But not only did Trump campaign on killing national and global climate action, he is filling his White House and cabinet agencies with a den of climate science deniers.

No surprise, then, that the New York Times warned in a front-page story late last month, “Homeowners are slowly growing wary of buying property in the areas most at risk, setting up a potential economic time bomb in an industry that is struggling to adapt.”

How big a time bomb? A 2014 Reuters analysis of this “slow-motion disaster” had this chart:

It’s a trillion-dollar bubble.

Once again, this raises a key question for all Americans: What year will coastal property values crash?

I first posed the question in 2009, pointing out that coastal property values will crash long before sea levels have actually risen a few feet. Instead, coastal property values will crash when a large fraction of the financial community, mortgage bankers and opinion-makers — along with a smaller but substantial fraction of the public — realize that it is too late for us to stop catastrophic sea level rise.

When sellers outnumber buyers, and banks become reluctant to write 30-year mortgages for doomed property and insurance rates soar, then the coastal property bubble will slow, peak, and crash.

This appears to be underway. As the Times reports, “Nationally, median home prices in areas at high risk for flooding are still 4.4 percent below what they were 10 years ago, while home prices in low-risk areas are up 29.7 percent over the same period, according to the housing data.” Since 2001, “home sales in flood-prone areas grew about 25 percent less quickly than in counties that do not typically flood.”

South Miami mayor Philip Stoddard warns that “coastal mortgages are growing into as big a bubble as the housing market of 2007.” But, he notes, when this bubble crashes it will never recover. Indeed, property values will keep declining since the waters will keep rising and the storm surges will only get worse.

Back in April, Sean Becketti, the chief economist for mortgage giant Freddie Mac also warned this scenario is much closer than the public realizes, in a post and video sardonically headlined, “Life’s a beach.”

In the post, Becketti contemplates when the value of a beachfront house will start to crash. “Will the value of the house decline gradually as the expected life of the house becomes shorter? Or, alternatively, will the value of the house — and all the houses around it — plunge the first time a lender refuses to make a mortgage on a nearby house or an insurer refuses to issue a homeowner’s policy?”

His bottom line: “Some residents will cash out early and suffer minimal losses. Others will not be so lucky.”

Again, the question is: When will the smart money walk away?

Back in 2009, there were multiple studies suggesting sea level rise in 2100 would be 3 to 6 feet. Since then the evidence keeps getting stronger that, absent deep cuts in carbon pollution, we are heading to the high end of sea level rise — or even higher. Moreover, if we do hit 5 or 6 feet of sea level rise this century, seas will keep rising some one foot or more per decade.

Just this year, the journal Nature published research that found “Antarctica at Risk of Runaway Melting,” as Climate Central put it. A detailed model of the Antarctic ice sheet found “up to 6 feet of sea level rise could result by the year 2100 if we keep increasing our greenhouse gas emissions,” climate expert Stefan Rahmstorf told me at the time. “The new study shows once again how urgent it is to reduce greenhouse gas emissions drastically in order to prevent a catastrophic sea level rise.”

With aggressive national and global CO2 cuts, that study found it’s possible Antarctica will contribute very little to the rate of sea level rise by 2100. But in the business-as-usual case — the policies Trump campaigned on — Antarctic ice loss by itself could be raising seas a staggering inch per year within the century.

To be clear, though, the 5 to 6 feet of sea level rise is not the worst-case scenario. For instance, it doesn’t include a more dynamic modeling of what will happen to Greenland’s ice sheet.

And brand new research just published in Nature finds that the Greenland ice sheet is actually much more unstable than most scientists thought. As a result, “global warming could tip it into decline more precipitously than previously thought,” the news release explains. “Such a decline could cause rapid sea-level rise.”

One paleoclimatologist not involved in the study said simply, “We can now reject some of the lowest sea-level projections.”

News from the Arctic and Antarctic is alarming. What’s about to happen in Washington, D.C. with the Trump presidency is even more alarming, all but guaranteeing the worst-case scenarios will play out.

And so the question for coastal property owners and financial institutions is: Who will be the smart money that gets out early — and who will be the other kind of money?